Outcry as Iran’s stock exchange officials secure cheap personal loans

Iran's Securities and Exchange Organization headquarters in Tehran

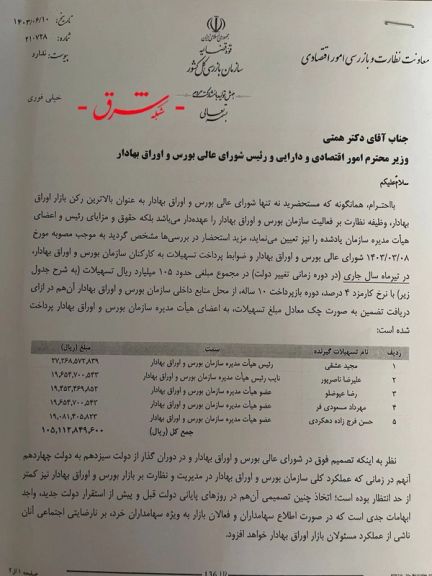

Exposing Iran’s ruling elite, the pro-reform Shargh daily has revealed a letter detailing how five officials appointed under President Ebrahim Raisi granted themselves loans totaling 105 billion rials ($175,000).

The officials, members of the Supreme Council of the Stock Exchange, orchestrated the generous loans with lenient repayment periods and minimal interest rates while Iran’s economy remains on the brink of collapse.

Majid Eshghi, Chairman of the Board of the Securities and Exchange Organization, received the largest loan, 27 billion rials ($45,000), with just 4% interest over a 10 year period. To put this amount in perspective, and ordinary worker in Iran earns just $200 a month.

A sample page of the letter published by Shargh Daily

The loans were approved during the final days of the Raisi government, bypassing orders from both acting president Mohammad Mokhber and president-elect Masoud Pezeshkian. Experts warn that the move threatens to destabilize Iran’s capital market by further eroding investor confidence.

Other council members, including Alireza Nasserpour, Reza Eivazlou, Mehrdad Masoudifar, and Hassan Farajzadeh Dehkurdi, each received 19 billion rials (over $31,000) in loans.

On Thursday, Abdolnasser Hemmati, Iran’s Minister of Economy, announced the launch of an “urgent expert review” into the scandal. Many view this as a mere formality, with little expectation of accountability in a system where officials have long shielded themselves from public scrutiny.

Iman Aghayari, a political activist, told Iran International that corruption in Iran has evolved into a kleptocracy, becoming ingrained as a behavioral model. “At the top, there is a person [Ali Khamenei] who treats the entire country as his personal property, and at the lower levels, others believe they must plunder the limited resources available to them," he said.

Iran’s Central Bank is already under fire for reports of astronomical loans being granted by major banks to their own employees and subsidiaries. According to a report released by the Central Bank last week, these institutions funneled over 9,100 trillion rials ($1.5 billion) in loans to their employees, managers, and board members in 2023 alone.

The Central Bank of Iran headquarters in the capital Tehran

Two of the most politically influential banks, Mellat and Sepah, are the lead suspects, both notorious for their involvement in Tehran’s military and nuclear programs, which have brought crippling international sanctions upon Iran. Mellat Bank alone issued 190 trillion rials ($315 million) in loans to its subsidiaries last year, with Sepah Bank not far behind, distributing 145 trillion rials ($240 million).

Not only are these government banks controlled by regime insiders, but their subsidiary companies also serve as strongholds for political appointees and nepotism.

In contrast, ordinary Iranians face challenges securing loans for housing, marriage, or entrepreneurship, with delays and denials becoming the norm. Marriage loans, crucial for thousands of young couples, have been sidelined, while bank employees are handed fortunes with ease.

The disparity in access to loans is vast between Iran's elite and the ordinary citizen. For bank employees, loan ceilings can reach over 10 billion rials ($16,000), while retirees, struggling to survive on meagre pensions, are limited to loans of just 300 million rials ($500). Meanwhile, tenants and entrepreneurs face long waiting lists as banks cite financial shortfalls.

Around one in three Iranians now lives below the poverty line as inflation has exceeded 40% for the last five years leaving many struggling with basic costs such as food and housing.

The White House convened a meeting with representatives of Amazon, Alphabet's Google, Microsoft, Cloudflare and civil society activists on Thursday in a bid to encourage US tech giants to offer more digital bandwidth for government-funded internet censorship evasion tools.

The tools, supported by the US-backed Open Technology Fund (OTF), have seen a surge of usage in Russia, Iran, Myanmar and authoritarian states that heavily censor the internet.

OTF's pitch to tech companies at the meeting was to help offer discounted or subsidized server bandwidth to meet the fast-growing demand for virtual private network (VPN) applications that OTF funds, the organization’s president, Laura Cunningham, told Reuters.

“Over the last few years, we have seen an explosion in demand for VPNs, largely driven by users in Russia and Iran,” Cunningham said. “For a decade, we routinely supported around nine million VPN users each month, and now that number has more than quadrupled.”

VPNs help users hide their identity and change their online location, often to bypass geographic restrictions on content or to evade government censorship technology, by routing internet traffic through external servers outside of that government’s control.

The US government launched its first Internet blockage circumvention tool in 2009 when the Iranian government expanded its censorship during anti-government protests. Later, the OTF was created to oversee and coordinate the US government’s Internet anti-censorship effort, annually receiving around $15 million in mid-2010s.

Iranians have long been the biggest users of the US-provided and other VPNs, since thousands of websites and all major social media applications are blocked by the government both for political and religious purposes.

The OTF specifically backs VPNs that are designed to work in states that restrict access to the internet. The U.S. injected increased funding into VPNs supported by the OTF following Russia’s invasion of Ukraine in 2022, Reuters reported at the time.

The organization has since received a boost to its budget from the US State Department via its “Surge and Sustain Fund for Anti-Censorship Technology”, an initiative created at the Biden administration’s Summit for Democracy.

But it has struggled to meet increased demand in countries like Russia, Myanmar, and Iran, where internet censorship heavily restricts access to outside information.

Around 46 million people a month now use US-backed VPNs, Cunningham said, but added that a sizeable chunk of the budget was taken up by the cost of hosting all that network traffic on private sector servers.

“We want to support these additional users, but we don't have the resources to keep up with this surging demand,” she said.

Representatives of Amazon Web Services, Google, and Microsoft did not immediately respond to a request from Reuters for comment.

A Cloudflare spokesperson said the firm was working with researchers to "better document internet shutdowns and censorship."

New details have emerged surrounding the Iranian plot to kill ex-President Donald Trump, claiming that Iran targeted "politicians, military people or bureaucrats" including President Joe Biden and former Republican presidential candidate Nikki Haley.

Senator Chuck Grassley released whistleblower information from FBI records amid Trump’s latest presidential bid and in the wake of a failed assassination attempt against Trump just weeks ago, which Iran denied links to.

In a statement, Grassley said: ”Bad actors are determined to wreak havoc on our country, and American political leaders across both parties are sitting squarely in the crosshairs.

“In this extraordinarily heightened threat environment, federal agencies ought to be laser focused on building up public trust and reassuring the American people of their efforts to carry out their protective missions."

He vowed he will not "stop pressing for answers until Congress and the American people are afforded the transparency they deserve.”

Asif Merchant, a Pakistani with known ties to Iran, has been charged for his involvement and according to the FBI documentation, provided evidence to the FBI in a plea deal. He was arrested just one day before the July assassination attempt.

Asif Merchant

According to the FBI records, Merchant believed he was in for a kill-for-hire scheme that would offer him a cut of $50,000 for successful completion. He had told FBI interrogators that there were options for shooting former President Trump at both indoor and outdoor speaking engagements.

The Pakistani, 46, told investigators that he could hit a target up close or from further away, that a pistol would be best for indoors, but a rifle was necessary otherwise. He is said to have believed he had about a 50% chance of success.

English language notes were smuggled by Merchant’s family members to communicate with his handlers in Iran.

While the FBI has still not commented on the July assassination attempt on Trump by Thomas Matthew Crooks, while investigations continue, the option of it having been an Iranian plot has not been ruled out.

Security had been increased in June based on intelligence suggesting plots to kill him as Iran continues to vow revenge for Soleimani, killed in a drone strike in Iraq in 2020, ordered by Trump for his involvement in terror targeting US troops.

According to the justice department's indictment, Merchant arrived in the US from Pakistan in April after having spent time in Iran, when he contacted someone he thought would help him enact the plot. The unnamed contact reported him to the authorities.

Merchant had apparently told the contact he would leave the US before the killings, staying in contact only through code words.

FBI director Christopher Wray called the scheme a "dangerous murder-for-hire plot... straight out of the Iranian playbook".

Last year, the US listed Iran as the world's number one state sponsor of terrorism while plots to kill dissidents, Israeli and Jewish targets around the world have become increasingly more common.

Demanding transparency from security agencies, Grassley said that a DHS-FBI briefing from earlier this week "yet again failed to provide full transparency, necessitating this letter and the public disclosure of the unclassified proffer.”

Kayhan’s daily’s frequent attacks on pro-reform and even hardline governments is well known in Tehran. However, many agree that the hardline paper has launched its offensive against the Pezeshkian administration unusually early.

Kayhan and its managing editor, Hossein Shariatmadari, began attacking Pezeshkian even before his cabinet was finalized. Shariatmadari criticized the president's selection of ministers early on, targeting his choices before they were officially confirmed. He went further, accusing Pezeshkian of appointing aides and vice presidents who he labeled "political criminals" and supporters of "seditionists" — a term referring to those who backed popular protests.

A report on Etemad Online website on Wednesday suggested that Hossein Shariatmadari has undergone a "factory reset," returning to his familiar tactic of launching destructive attacks on the president and his administration. The report followed Shariatmadari’s accusation that the Pezeshkian administration has deviated from its commitment to Khamenei’s ideals.

Under Shariatmadari, Kayhan has worked hard to present itself as a media outlet closely aligned with Khamenei’s views. However, this portrayal is not entirely accurate, as other newspapers, such as Ettela'at, Jomhouri Eslami, and Khorasan, are also financially and editorially linked to Khamenei’s office yet maintain different editorial perspectives. This diversity of viewpoints among pro-Khamenei outlets highlights a complex media strategy by the Supreme Leader.

In several reports Iranian journalists and politicians pointed out that what Kayhan writes solely reflects Shariatmadari's ideas and biases rather than reflecting Khamenei's views. Others believe that the paper has a function of being the ‘attack dog’ for Khamenei’s court.

According to Etemad Online, Kayhan's attacks on Pezeshkian seem particularly strange given Khamenei’s favorable stance toward the new president and his cabinet. In recent instances, Khamenei has personally shown support for figures like Vice President Zarif and Health Minister Zafarghandi, who were both targets of Shariatmadari's harsh criticism. This disconnect between Kayhan's hostility and Khamenei's approval raises questions about the motivations behind the newspaper's stance.

The Kayhan whose line of thought often resembles those of ultraconservative Paydari Party pretended that the Pezeshkian administration faces no financial shortages. This was refuted by the President during an interview with the state TV in which he said his government had no funds in the Treasury and he had to borrow money from the National Development Fund to start his work.

In summary, Kayhan's opposition to the Pezeshkian administration centers on several key issues: Shariatmadari's criticism of Pezeshkian's decision to reinstate academics and students dismissed for supporting the 2022 protests, his objections to the appointment of Abbas Araghchi as Foreign Minister and the inclusion of former officials like Javad Zarif in the cabinet, and his negative views toward two reformist-leaning ministers. This broad opposition reflects Kayhan's discontent with Pezeshkian’s choices.

In another report on Wednesday, Etemad Online quoted reformist activist Mohammad Reza Jalaipour, who refuted Kayhan's claims, stating that neither Khamenei's Office nor the IRGC have plans to confront the Pezeshkian administration. He emphasized that the new government is a result of a "win-win" collaboration between the executive branch and Khamenei’s office. Jalaipour expressed optimism about the government's future, noting the Supreme Leader's support.

Meanwhile, an online campaign is calling for Shariatmadari’s resignation, suggesting he’s "tired after 30 years of hard work."

The shift in Moscow’s policy regarding the Zangezur corridor through Armenia has angered Tehran where some see Vladimir Putin’s move as an attempt to prevent improvement in Tehran’s relations with the US.

Baku has been demanding a corridor through southern Armenia to connect Azerbaijan to its Nakhchivan enclave separated by Armenian territory.

As commentators and pundits in Tehran were criticizing Russian policy this week, Foreign Minister Abbas Araghchi issued a post on X on Thursday saying, "Regional peace, security and stability is not merely a preference, but a pillar of our national security. Any threat from North, South, East, or West to territorial integrity of our neighbors or redrawing of boundaries is totally unacceptable and a red line for Iran."

Moscow and Baku want Russia to monitor and control the corridor which can serve as a significant route for trade and energy transport between Asia and Europe, but Yerevan and Tehran are opposed to such a scheme and argue that even if a transport route were to be established, Armenia should have control over it.

Former chairman of the Parliament’s National Security and Foreign Policy Committee, Heshmatollah Falahatpisheh, claimed in a Thursday X post that Russian President Vladimir Putin’s push for the establishment of the Zangezur corridor is a “preemptive move” to pressure Iran. According to Falahatpisheh, this is intended to deter Pezeshkian's government from opening "communication channels" with Washington.

Putin is aware that, despite Iran’s failed pro-Russia and pro-China policy, the key message of the recent presidential election was a call for de-escalation in relations with the West and a move away from dependence on Eastern powers, he argued.

Similarly, Iranian journalist Maryam Salari argues that Moscow's disregard for Tehran’s opposition to the Zangezur corridor must be understood in the context of Masoud Pezeshkian's election and his emphasis on negotiating with the West to lift U.S. sanctions.

“Raisi's Eastward-focused foreign policy had reassured Putin about Iran’s stance, but Pezeshkian's candidacy and his pledge to prioritize negotiations with the West to lift sanctions have unsettled Russia's regional plans,” Salari posted on X.

Russia’s prolonged delay in signing a 20-year comprehensive cooperation agreement with Iran, despite the support Iran has provided in the Ukraine conflict, has increasingly frustrated the Islamic Republic. This hesitation from Moscow has sparked irritation in Tehran, especially given the significant assistance Iran has offered.

“Russia has never cared about Iran's interests … This corridor blocks Iran's access to Europe through Armenia,” the conservative former lawmaker Ali Motahari tweeted Thursday and urged the government of Masoud Pezeshkian to be “perceptive” regarding the establishment of Zangezur corridor.

Tehran recently summoned the Russian Ambassador, Alexi Dedov, to the foreign ministry over the matter and congratulated Ukraine last month on its independence day. The move could be interpreted as an overture to Ukraine and an affront to Russia, according to some pundits.

In an editorial Thursday entitled “Russia’s Geopolitical Coup Against Iran”, the reformist Arman-e Emrooz daily criticized the foreign ministry’s reaction to Russia’s insistence on establishing the corridor.

“The foreign ministry’s reaction has not been sufficiently decisive and deterrent despite the irreparable damage caused by Russia's position which practically leads to the geopolitical suffocation of Iran at its the northern borders,” Arman-e Emrouz contended.

Not only reformists but also the media linked with the Revolutionary Guard have been criticizing the shift in Moscow’s policy.

“Russia has been also advised to avoid taking measures that may impair the strategic relations between Moscow and Tehran, because the idea of the Zangezur corridor will create a new flashpoint near the very delicate boundaries of northwestern Iran,” the Revolutionary Guards (IRGC) linked Tasnim news agency warned Wednesday in an editorial on its English portal.

The Persian version of Tasnim’s editorial on the subject was stronger in tone, stressing that “Iran will not accept any changes in its borders and its security peripheries” and underlines that “confronting international bullies is a fundamental strategy” of the Islamic Republic. The editorial also called the corridor “imaginary” and reminded the summoning of the Russian ambassador.

Iranian journalist Mohammad Parsi also took to X to protest that the Islamic Republic still considers Russia as a “friend and strategic ally” althoughMoscow sided with Saddam Hussein in his war against Iran, stood alongside the United States when the UN Security Council passed resolutions against Iran, supported European sanctions, and supports Azerbaijan’s demand regarding Zangezur. “What does this mean?” he asked.

“Russia’s illusions and problems should not distract our country from its own national interests,” Hadi Mohammadi, another Iranian journalist, posted on X.

A series of Iranian-backed terror plots targeting Jews and Israeli-linked businesses in Europe were foiled by security services earlier this year, according to an investigation by the German daily Der Spiegel.

The thwarted attacks, planned for 2024, involved a criminal network recruited by Tehran to conduct surveillance on Jewish and Israeli targets in Germany. At the same time, a series of arson attacks targeted Israeli-owned businesses in southern France, starting at the end of 2023 and continuing into 2024.

Iran International reported In May this year that Israeli and Swedish Intelligence agencies warned about Iran using criminal networks as terrorist proxies in Europe to carry out a string of attacks on Israeli embassies in Europe since October 7.

Planned attacks against Jewish and Israeli targets in Germany

According to the report, one of the key suspects who is referred to as Abdolkarim S., is a 34-year-old French national with a history of violent crime. Abdolkarim, known for his involvement in the drug trade in Marseille, was allegedly recruited by Tehran to scout Jewish and Israeli-related targets in Europe.

In February 2024, Abdolkarim and his wife traveled to Berlin, where, according to German investigators, he used his wife's phone to locate the office of a Jewish lawyer who represents Israeli clients. Investigators found the address of the lawyer’s office on a navigation app used during the trip. This marked the first appearance of the Iranian-sponsored cell in Germany.

Two months later, in April 2024, Abdolkarim made two separate trips to Munich, this time without his wife. According to Der Spiegel, German security services closely monitored him as he scouted a Jewish family’s business in the eastern part of Munich. He filmed the building, its surroundings, and doorbell signs. Investigators suspect the family, which has close ties to Israel, was the intended target of a planned attack. In one audio message sent to an unknown recipient, Abdolkarim reportedly said, “I have seen the company, there were people inside, but the person wasn’t there,” suggesting he had been scouting for a specific individual.

These surveillance activities did not go unnoticed. German intelligence services tracked Abdolkarim’s movements, leading to his arrest in late April 2024. Abdolkarim was subsequently detained in France, and French authorities have charged him with terrorism-related offenses. His surveillance efforts in Germany are believed to have been part of a broader plan by Tehran to orchestrate attacks against Jewish and Israeli figures in Europe.

Arson attacks on Israeli-owned businesses in France

While the attacks in Germany were thwarted, Israeli-owned businesses in southern France were targeted in a series of arson attacks. Between December 2023 and January 2024, four businesses were set on fire, including a warehouse near Montpellier. The businesses ranged from a water treatment company to a software engineering firm, which on the surface appeared to have little in common. However, investigators, according to Der Spiegel, discovered that all the companies were owned by Israelis, linking the attacks to the same criminal network associated with Abdolkarim.

French intelligence agency DGSI believes the arson attacks were part of a larger Iranian plot to strike Israeli-linked interests in Europe. Investigators reportedly found the addresses of the targeted businesses on Abdolkarim’s phone, suggesting his role in passing the information to those who carried out the attacks. However, the physical perpetrators of the arson attacks have not yet been identified.

Tehran’s use of criminal networks

Western intelligence agencies have been tracking an emerging trend where the Iranian regime uses criminal networks in Europe to carry out state-sponsored terrorism. Tehran has shifted its strategy in recent years, moving away from using its own agents and instead relying on local criminals to execute terror attacks, as reported by Der Spiegel. This approach, security officials suggest, allows Iran to maintain “deniability” by distancing itself from direct involvement.

The thwarted attacks in Germany and the arson in France are part of this broader pattern. Abdolkarim was released from prison in 2023 after serving time for his role in a gang murder. Shortly after his release, he was allegedly recruited by Tehran’s network.

Despite the arrests, investigators remain concerned that media reports revealing the Iranian-backed plot in April may have compromised their efforts to fully dismantle the terror cell.